With VIX near 20 and breadth fading, are rallies now shortable gifts?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-06-08

Executive Summary Date: 2026-06-09

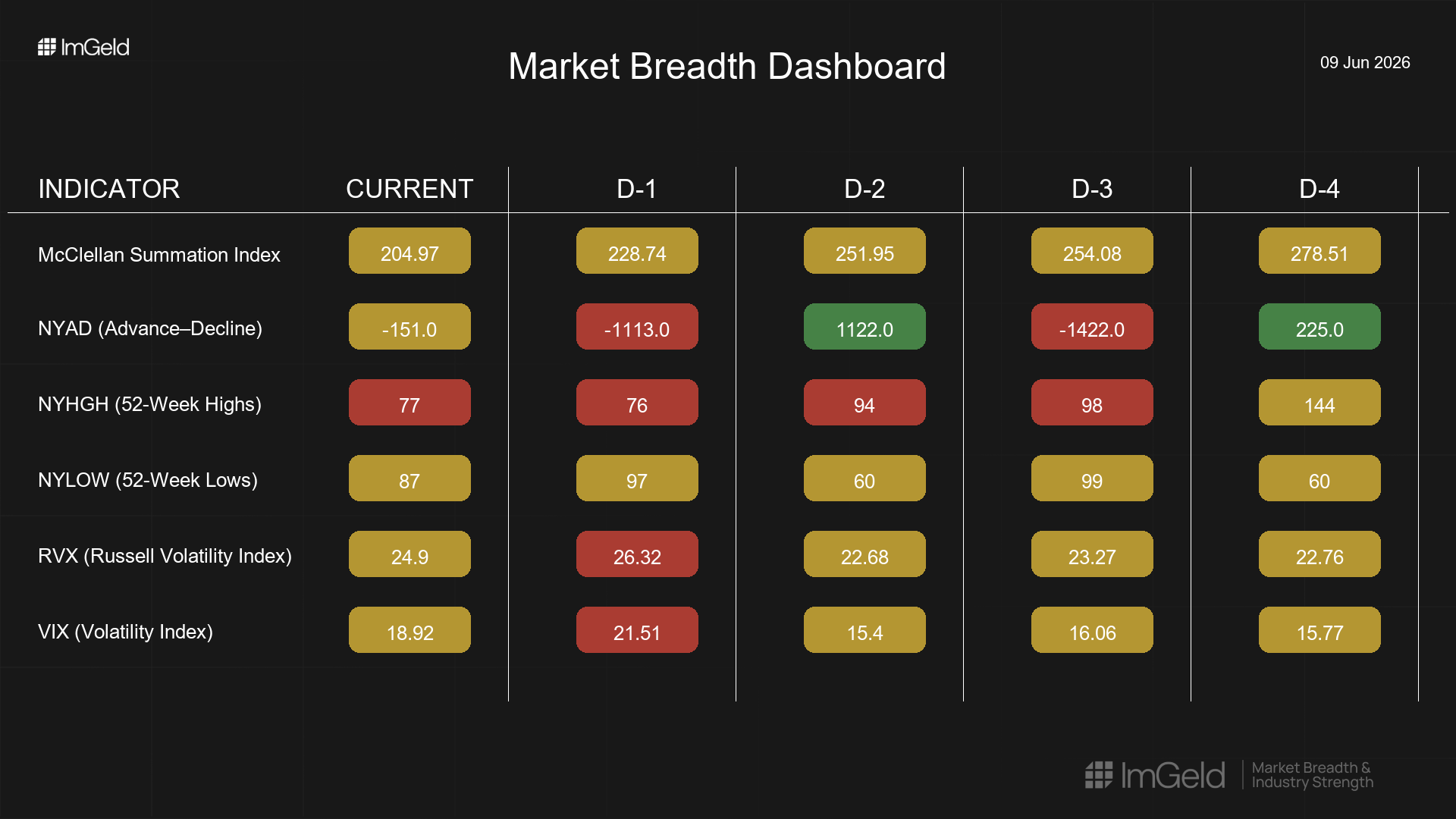

Breadth weakened over the last five sessions. NYSI (McClellan Summation Index) declined each day, while NYAD (Advance–Decline Line) whipsawed with a downside skew. Volatility expanded, with VIX (CBOE Volatility Index) spiking toward 21 before settling in the high teens, and RVX (Russell Volatility Index) holding in the mid-20s.

Tactically, maintain a neutral bias with elevated selectivity. Emerging opportunities are limited to selective mid-cap longs in resilient, cash-generative industries that are defending relative strength and showing muted participation in new lows. Short setups remain valid in crowded large-cap leadership where momentum is faltering, particularly in high-beta growth industries; favor entries on rallies

.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation is firmly narrowing over the five-day window: NYSI fell consistently, NYHGH (New 52-Week Highs) trended lower, and NYLOW (New 52-Week Lows) stayed elevated. Leadership is becoming more concentrated and showing signs of rotation toward defensive and quality profiles rather than broad expansion. Volatility is firmly expanding. A mild divergence exists as NYSI trended down while NYAD oscillated; the bounce in NYAD failed to arrest the NYSI decline, signaling weak underlying thrust. The five-day pattern indicates continuation of distribution rather than early accumulation.

Indicator Breakdown

NYSI (McClellan Summation Index) Firm deterioration across all five sessions (278.51 to 204.97). No evidence of basing; intermediate breadth impulse is weakening.

NYAD (Advance–Decline Line) Mixed but net negative: +225, -1422, +1122, -1113, -151. Positive thrusts were countered by heavier down-day breadth, indicating sellers retain control on pressure days.

NYHGH (New 52-Week Highs) Leadership contraction from 144 to 77. Fewer leaders are carrying performance, underscoring concentration risk.

NYLOW (New 52-Week Lows) Persistent elevation (60 to 87) with two spikes, reflecting ongoing downside pressure and softer risk appetite.

Volatility Regime VIX rose from mid-15s to a 21.51 spike before settling at 18.92; RVX moved from ~22.7 to 26.32 and remains elevated at 24.9. This expansion argues for disciplined sizing, tightened risk limits, and preference for mean-reversion entries over momentum chases.

Tactical Implications

Mid-cap long focus: selectively in industries with defensive cash flows and relative strength (e.g., specialty insurance, waste services, diversified healthcare distributors), favoring pullback entries where new-lows participation is subdued.

Large-cap shorts: maintain on rallies in crowded leadership within high-beta growth industries (e.g., semiconductors, application software, consumer internet) where breadth is narrowing and volatility is elevated.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.