With NYSI sliding and RVX re-rating, are semiconductor highs simply distribution into strength?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-06-10

Executive Summary Date: 2026-06-11

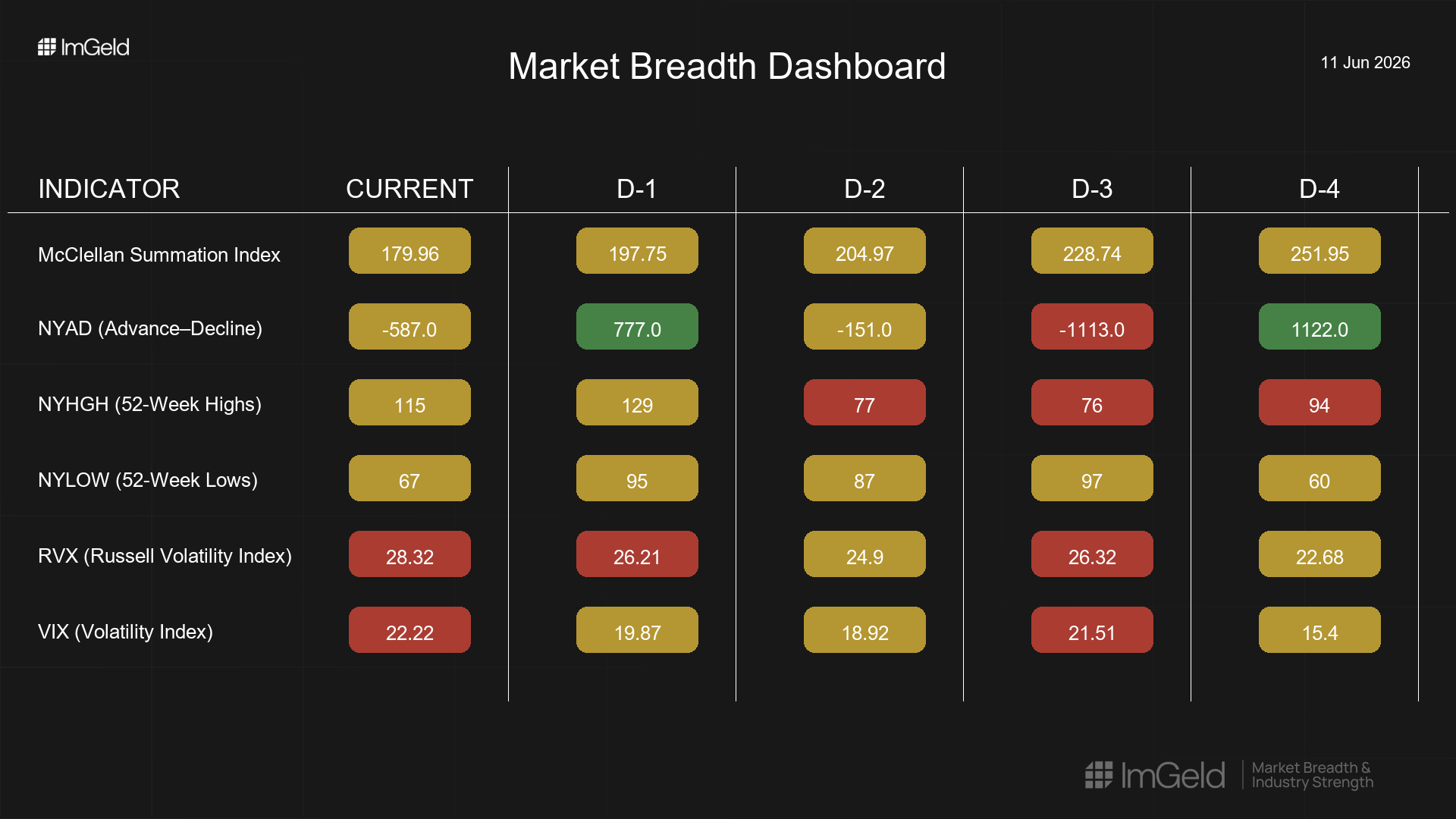

Breadth cooled over the last five sessions. NYSI (McClellan Summation Index) declined steadily, signaling intermediate-term deterioration despite remaining positive. NYAD (Advance–Decline Line) was choppy with alternating strong positive and negative days, indicating unstable participation. Volatility expanded as VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) both rose, reinforcing a risk-off tone and favoring selectivity.

Tactically, long opportunities are emerging only in mid-cap industries showing rising new highs and contained drawdowns, with emphasis on cash-flow defensive or idiosyncratic catalysts. Short setups remain valid in large-cap growth-heavy industries where leadership is narrow and overextended, particularly in semiconductors and software, with a preference to sell strength into volatility.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation is narrowing as NYSI fell in each of the last five sessions while NYAD oscillated, a divergence that points to underlying distribution rather than broad accumulation. Leadership is becoming more concentrated; NYHGH improved late in the period but looks clustered rather than widespread. Volatility is firmly expanding, as both VIX and RVX advanced from prior lows. The five-day pattern signals continuation of distribution pressure with intermittent relief rallies. By the five-day consistency rule: NYSI is firmly declining; NYAD remains mixed; volatility is firmly expanding; leadership broadening is tentative.

Indicator Breakdown

NYSI (McClellan Summation Index)

Declining across all five sessions (251.95 to 179.96). Structure is weakening, indicating a loss of intermediate momentum even as the level remains positive. A base is required before broad beta exposure is warranted.

NYAD (Advance–Decline Line)

Highly variable (+1122, -1113, -151, +777, -587). Participation is unstable and rotational, offering little confirmation to rallies and increasing the probability of failed breakouts.

NYHGH (New 52-Week Highs)

Rebounded late (94, 76, 77, 129, 115). Leadership pockets are expanding tentatively, likely concentrated in select mid-cap industries with defensible earnings visibility or event-driven support.

NYLOW (New 52-Week Lows)

Elevated mid-period with moderation into the latest session (60, 97, 87, 95, 67). Downside pressure persists but is easing, suggesting selective risk appetite rather than broad risk-on.

Volatility Regime

VIX rose from 15.4 to 22.22; RVX from 22.68 to 28.32. The expanding regime argues for tighter risk controls, preference for relative-value and pair constructs, and patience on entry timing.

Tactical Implications

Long: Focus only on mid-cap industries exhibiting rising new highs and relative strength, such as insurance, specialty chemicals, defense suppliers, and waste management, where dispersion and cash-flow resilience support stock-picking.

Short: Large-cap growth industries remain vulnerable given narrow leadership and higher volatility, notably semiconductors and software; favor selling strength and maintaining discipline on cover triggers.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.