Is VIX compression hiding a stealth breadth rotation that leaves mega-caps vulnerable?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-07-02

Executive Summary Date: 2026-07-03

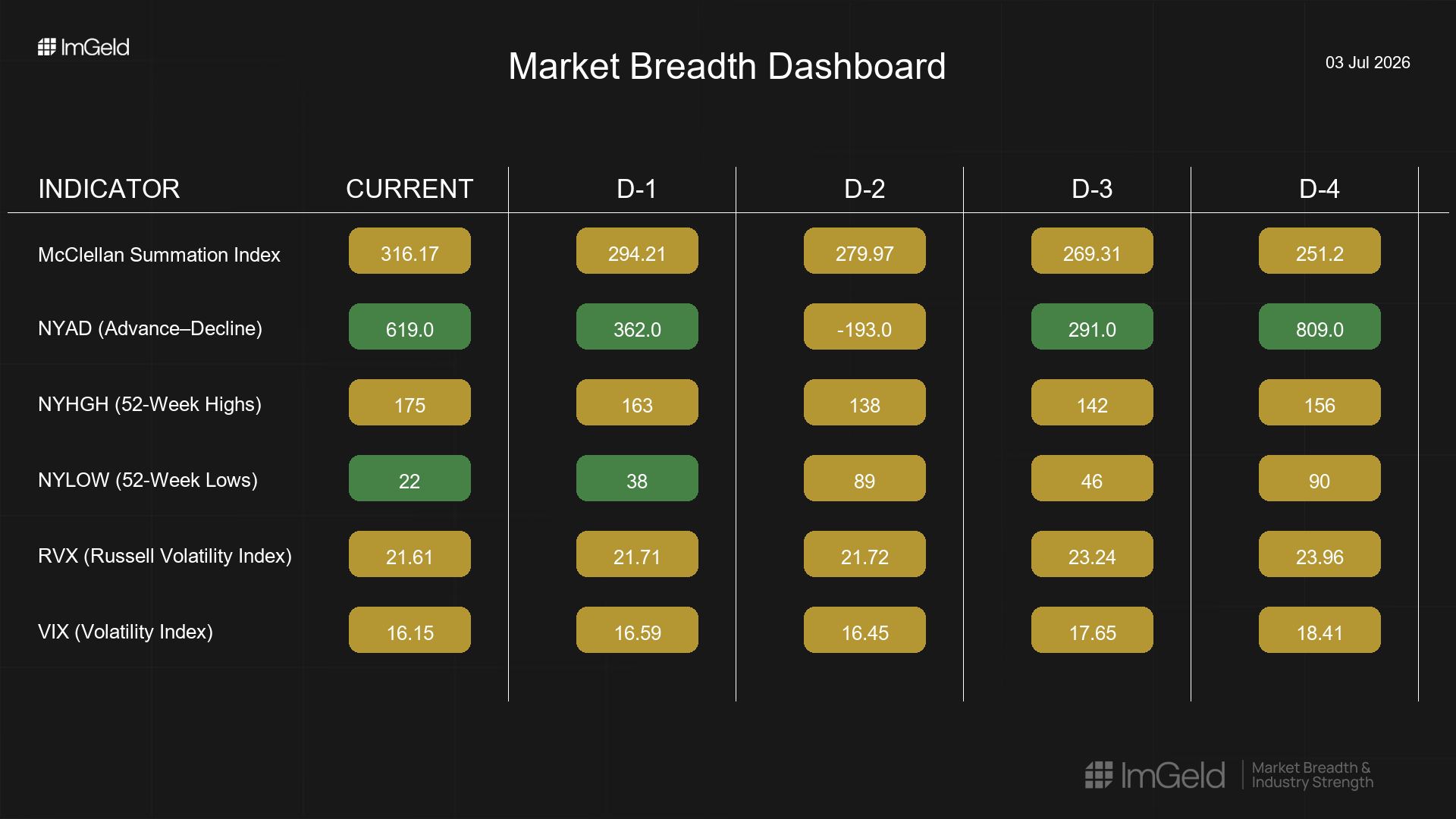

Breadth improved over the past five sessions despite a Tentative short bias. NYSI (McClellan Summation Index) advanced steadily from 251.2 to 316.2, while NYAD (Advance–Decline Line) printed positive on four of five days, signaling improving participation. Volatility compressed as VIX (CBOE Volatility Index) fell to 16.15 and RVX (Russell Volatility Index) eased to 21.61, indicating a calmer risk backdrop.

Tactically, improving breadth and compressing volatility argue for high selectivity. Long opportunities are emerging in mid-cap industries where new highs are expanding and new lows are contracting. Short opportunities remain more appropriate in large caps where leadership is over-owned and breadth lags. Selectivity is critical; favor pullbacks and defined-risk entries.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation is broadening, firmly evidenced by five consecutive NYSI gains and four positive NYAD sessions. Leadership shows early signs of expansion rather than concentration, with NYHGH (New 52-Week Highs) rebounding late in the week and NYLOW (New 52-Week Lows) collapsing to cycle lows. Volatility is compressing in both VIX and RVX, reducing tail hedging costs but increasing the risk of abrupt repricing on shocks. NYSI’s persistent rise versus a briefly negative NYAD on 06/30 reflects only a minor, isolated divergence. The five-day pattern points to early accumulation rather than exhaustion.

Indicator Breakdown

NYSI (McClellan Summation Index) Structure is firmly improving: five straight advances (251.2 → 316.2) with accelerating slope into week’s end, signaling strengthening intermediate breadth.

NYAD (Advance–Decline Line) Daily participation was net constructive: 809, 291, -193, 362, 619. The single down day is isolated (Tentative), while the sequence otherwise confirms strengthening breadth.

NYHGH (New 52-Week Highs) Leadership expansion is re-emerging: 156, 142, 138, 163, 175. The late-week pickup signals improving upside leadership consistent with accumulation.

NYLOW (New 52-Week Lows) Downside pressure is easing: 90, 46, 89, 38, 22. The sharp late-week compression in lows reflects improving risk appetite and reduced liquidation pressure.

Volatility Regime VIX declined from 18.41 to 16.15 and RVX from 23.96 to 21.61, a steady five-day compression. This backdrop favors continuation moves and disciplined carry, but mandates tight risk controls given the potential for sharp reversals from compressed volatility.

Tactical Implications

Longs: Prioritize mid-cap industries with improving breadth and rising new highs, such as industrial machinery, building products, specialty chemicals, regional banks, and specialty insurers. Enter on pullbacks; keep position sizing disciplined.

Shorts: Large-cap, index-heavy areas with narrow leadership and lagging breadth remain suitable for tactical fades on strength, notably select consumer internet platforms, mega-cap software, and integrated energy. Use defined-risk structures given low-volatility squeeze risk.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.