Are the RVX over VIX gap and rising NYLOWs flagging a failed accumulation attempt?

IMGELD Market Breadth Update Based on Last 5 Days Till the Data: 2026-06-19

Executive Summary Date: 2026-06-22

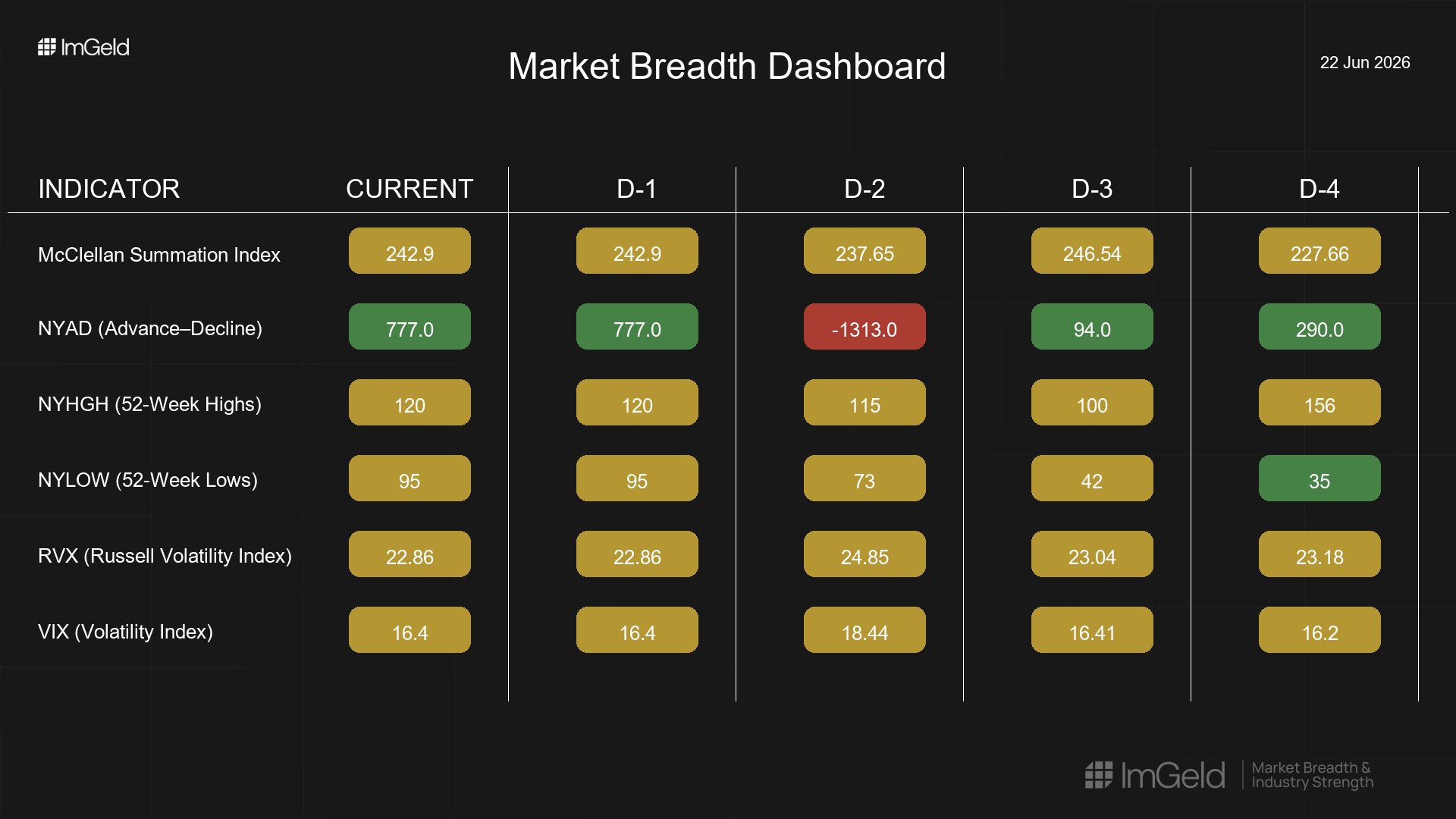

Breadth improved modestly but remained choppy over the last five sessions. NYSI (McClellan Summation Index) finished higher and flattened into the close of the week. NYAD (Advance–Decline Line) registered a sharp mid-week washout followed by two strong advances, leaving participation net positive but inconsistent. Volatility tone reset lower after a brief spike: VIX (CBOE Volatility Index) and RVX (Russell Volatility Index) reverted toward prior ranges.

Tactically, with a Neutral bias, prioritize selective long risk in mid-cap industries showing stable participation and relative strength. Short opportunities remain more valid in crowded large-cap leadership where highs failed to expand and breadth narrowed. Selectivity remains high given the rise in new lows.

.

Get the Industry Heat Map — delivered by email only.

Global Read

Participation remains mixed rather than broadly inclusive. Leadership is becoming more concentrated: NYHGH (New 52-Week Highs) failed to meaningfully expand, while NYLOW (New 52-Week Lows) trended higher through the week. Volatility expanded briefly mid-week and subsequently compressed, suggesting a fragile but contained risk backdrop. There is a mild divergence: NYSI’s net improvement contrasts with NYAD’s deep intraweek drawdown before recovery, signaling an unconfirmed base. By the five-day consistency rule, signals remain an early accumulation attempt, not yet firm.

Indicator Breakdown

NYSI (McClellan Summation Index) Net improvement from 227.7 to 242.9 with intraweek whipsaw. Structure is mildly constructive but plateaued into week-end, arguing for patience on adding risk.

NYAD (Advance–Decline Line) Daily prints of +290, +94, -1313, +777, +777 show a sharp breadth air pocket followed by two firm recovery days. Participation strengthened late but remains uneven.

NYHGH (New 52-Week Highs) 156 → 100 → 115 → 120 → 120. Leadership expansion is subdued; only a partial rebound, implying limited confirmation of upside attempts.

NYLOW (New 52-Week Lows) 35 → 42 → 73 → 95 → 95. Persistent rise highlights ongoing distribution pockets and constrained risk appetite beneath the surface.

Volatility Regime VIX lifted to 18.44 mid-week before reverting to 16.4; RVX peaked at 24.85 and eased to 22.86. The spike-and-fade pattern points to transient stress within a still-manageable regime. The RVX premium over VIX underscores higher idiosyncratic risk in smaller capitalizations; position sizing and staggered entries are preferred.

Tactical implications: emphasize selective longs in resilient mid-cap industries such as Aerospace and Defense suppliers, Specialty Chemicals, Electrical Equipment, Life Sciences Tools, and Property and Casualty Insurance. Consider shorts in large-cap, index-heavy leadership where momentum is extended and new highs failed to broaden, including Interactive Media, Semiconductor Design, and Technology Hardware industries.

Access the ImGeld Fundamental Report

Stay informed. Unlock the ImGeld Industry Updates — subscribers only.